Blab AI

S&P 500s Heavy Tech Tilt Raises Questions About Diversification as AI Momentum Wanes

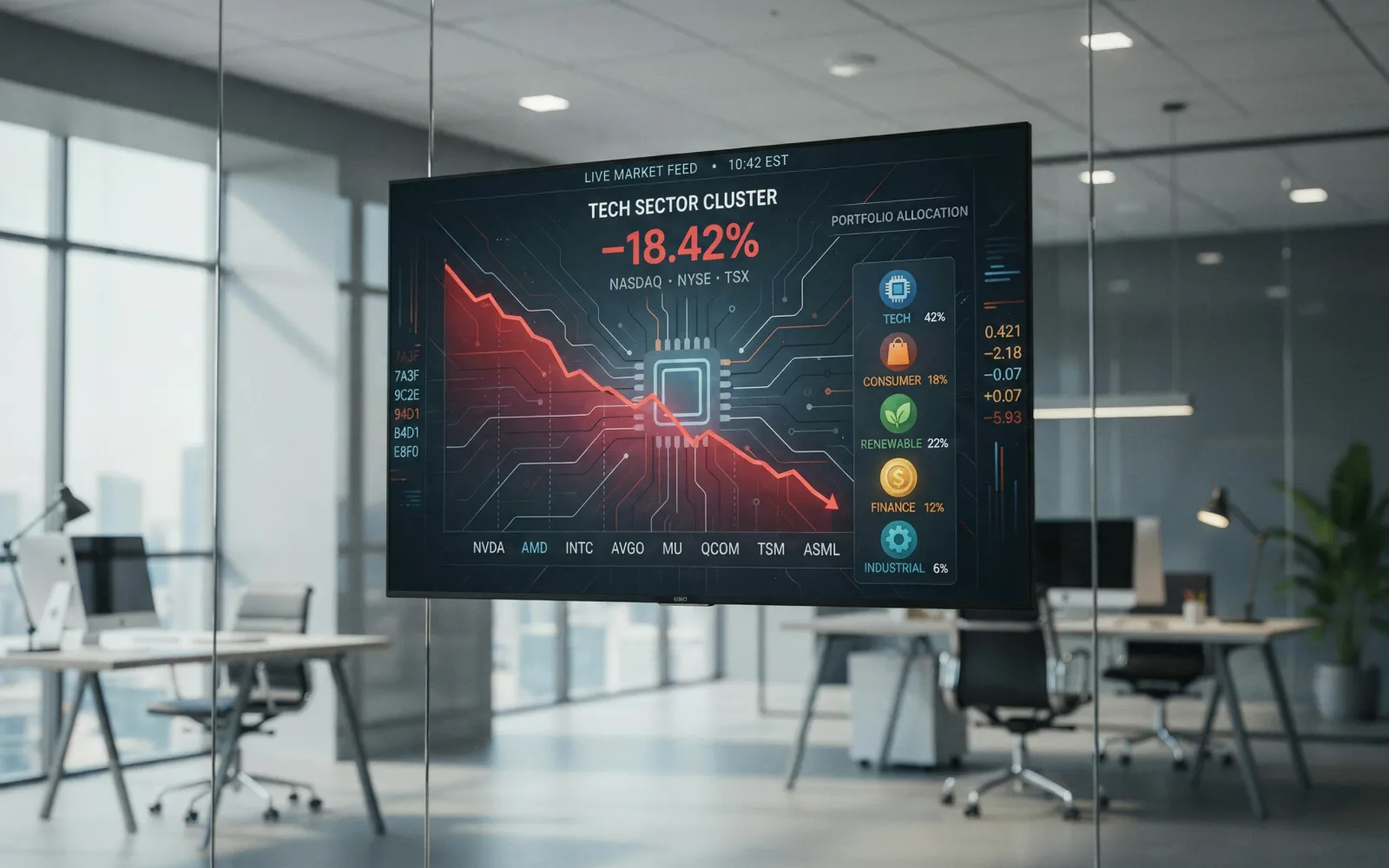

When you glance at the S&P 500, a single sector stands out: technology. Its 37 % weight, according to data cited by analyst Rob Isbitts, dwarfs the next largest group, Financials, at 12 %. The remaining ten sectors together make up the rest of the index, with Communication Services at 10 % and Consumer Discretionary and Health Care each at 9 %. Isbitts cautions that if the recent AI‑driven rally slows, the balance of the market will depend on the performance of these other groups.

Isbitts dissects the sector mix, labeling the Technology group—tracked by the XLK ETF—as the “absolute dictator” of the index because it is dominated by AI infrastructure and semiconductor leaders. He notes that the sector’s trajectory hinges on whether corporate buyers continue to pour money into R&D hardware, or whether a dip in enterprise AI spending forces a re‑rating.

Financials, represented by the XLF ETF, make up 12 % of the index. Their exposure to net interest margins and the sensitivity of loan‑loss provisions to short‑term rates are highlighted. Lower rates, potentially stemming from a reduction in geopolitical tensions, could lift banks, but persistent oil price spikes and inflationary pressures may still weigh on corporate earnings.

Communication Services, at 10 %, is driven by digital‑advertising and search giants. Its fortunes will depend on how effectively these firms weave generative AI into advertising, search, and streaming algorithms as consumer discretionary spending eases.

Consumer Discretionary, also 9 %, faces pressure from consumer elasticity. Retail, apparel, and automotive names are under strain as shoppers pull back on big‑ticket purchases.

Health Care, another 9 %, is undergoing a reset. After an initial focus on weight‑loss drugs, capital is returning to medical device makers, surgical suppliers, and hospitals as elective procedure backlogs grow.

Industrials, 10 % of the index, benefits from deglobalization, reshoring, and government spending, but higher borrowing costs and slower freight volumes present headwinds.

Consumer Staples, at 5 %, struggles with pricing power as input costs climb and consumers shift toward private‑label brands.

Energy, 3 % of the index, remains a wildcard. Supply deficits linked to the Strait of Hormuz could push oil prices higher, but the sector would need both higher prices and falling valuations in other areas to regain a larger share.

Utilities, 2 % of the index, has moved from a bond‑like profile to an AI‑infrastructure trade because data centers consume vast amounts of electricity.

Real Estate, also 2 %, is affected by the high‑interest‑rate environment and the need to refinance commercial debt.

Materials, 2 % of the index, is impacted by a global manufacturing slowdown and the challenge of offsetting de‑stocking with new infrastructure spending.

In the final section, Isbitts points to three ETFs that may offer steady gains in the near term: XLU (Utilities), XLP (Consumer Staples), and XLV (Health Care). He notes that XLU’s price oscillator has flattened, XLP’s individual holdings may perform better than the ETF’s overall weight, and XLV’s medical‑device sub‑sector could drive a broader rally.

The author concludes that while no sector ETF currently appears “thrilling,” the trio of XLU, XLP, and XLV represent potential slow‑but‑steady climbers. He emphasizes that investors should monitor the S&P 500’s sector composition rather than focusing solely on the index as a whole.

Isbitts created the ROAR Score, a technical‑analysis tool for DIY investors, and maintains the website ETFYourself.com. He states that he held no positions in the securities discussed at the time of publication.

The article provides a snapshot of the S&P 500’s sector weights and highlights the potential impact of a slowdown in AI‑driven growth on the broader market.

Isbitts dissects the sector mix, labeling the Technology group—tracked by the XLK ETF—as the “absolute dictator” of the index because it is dominated by AI infrastructure and semiconductor leaders. He notes that the sector’s trajectory hinges on whether corporate buyers continue to pour money into R&D hardware, or whether a dip in enterprise AI spending forces a re‑rating.

Financials, represented by the XLF ETF, make up 12 % of the index. Their exposure to net interest margins and the sensitivity of loan‑loss provisions to short‑term rates are highlighted. Lower rates, potentially stemming from a reduction in geopolitical tensions, could lift banks, but persistent oil price spikes and inflationary pressures may still weigh on corporate earnings.

Communication Services, at 10 %, is driven by digital‑advertising and search giants. Its fortunes will depend on how effectively these firms weave generative AI into advertising, search, and streaming algorithms as consumer discretionary spending eases.

Consumer Discretionary, also 9 %, faces pressure from consumer elasticity. Retail, apparel, and automotive names are under strain as shoppers pull back on big‑ticket purchases.

Health Care, another 9 %, is undergoing a reset. After an initial focus on weight‑loss drugs, capital is returning to medical device makers, surgical suppliers, and hospitals as elective procedure backlogs grow.

Industrials, 10 % of the index, benefits from deglobalization, reshoring, and government spending, but higher borrowing costs and slower freight volumes present headwinds.

Consumer Staples, at 5 %, struggles with pricing power as input costs climb and consumers shift toward private‑label brands.

Energy, 3 % of the index, remains a wildcard. Supply deficits linked to the Strait of Hormuz could push oil prices higher, but the sector would need both higher prices and falling valuations in other areas to regain a larger share.

Utilities, 2 % of the index, has moved from a bond‑like profile to an AI‑infrastructure trade because data centers consume vast amounts of electricity.

Real Estate, also 2 %, is affected by the high‑interest‑rate environment and the need to refinance commercial debt.

Materials, 2 % of the index, is impacted by a global manufacturing slowdown and the challenge of offsetting de‑stocking with new infrastructure spending.

In the final section, Isbitts points to three ETFs that may offer steady gains in the near term: XLU (Utilities), XLP (Consumer Staples), and XLV (Health Care). He notes that XLU’s price oscillator has flattened, XLP’s individual holdings may perform better than the ETF’s overall weight, and XLV’s medical‑device sub‑sector could drive a broader rally.

The author concludes that while no sector ETF currently appears “thrilling,” the trio of XLU, XLP, and XLV represent potential slow‑but‑steady climbers. He emphasizes that investors should monitor the S&P 500’s sector composition rather than focusing solely on the index as a whole.

Isbitts created the ROAR Score, a technical‑analysis tool for DIY investors, and maintains the website ETFYourself.com. He states that he held no positions in the securities discussed at the time of publication.

The article provides a snapshot of the S&P 500’s sector weights and highlights the potential impact of a slowdown in AI‑driven growth on the broader market.