Blab AI

AI Stock Retreat Highlights Growing Concerns Over Valuations and Long-Term Returns

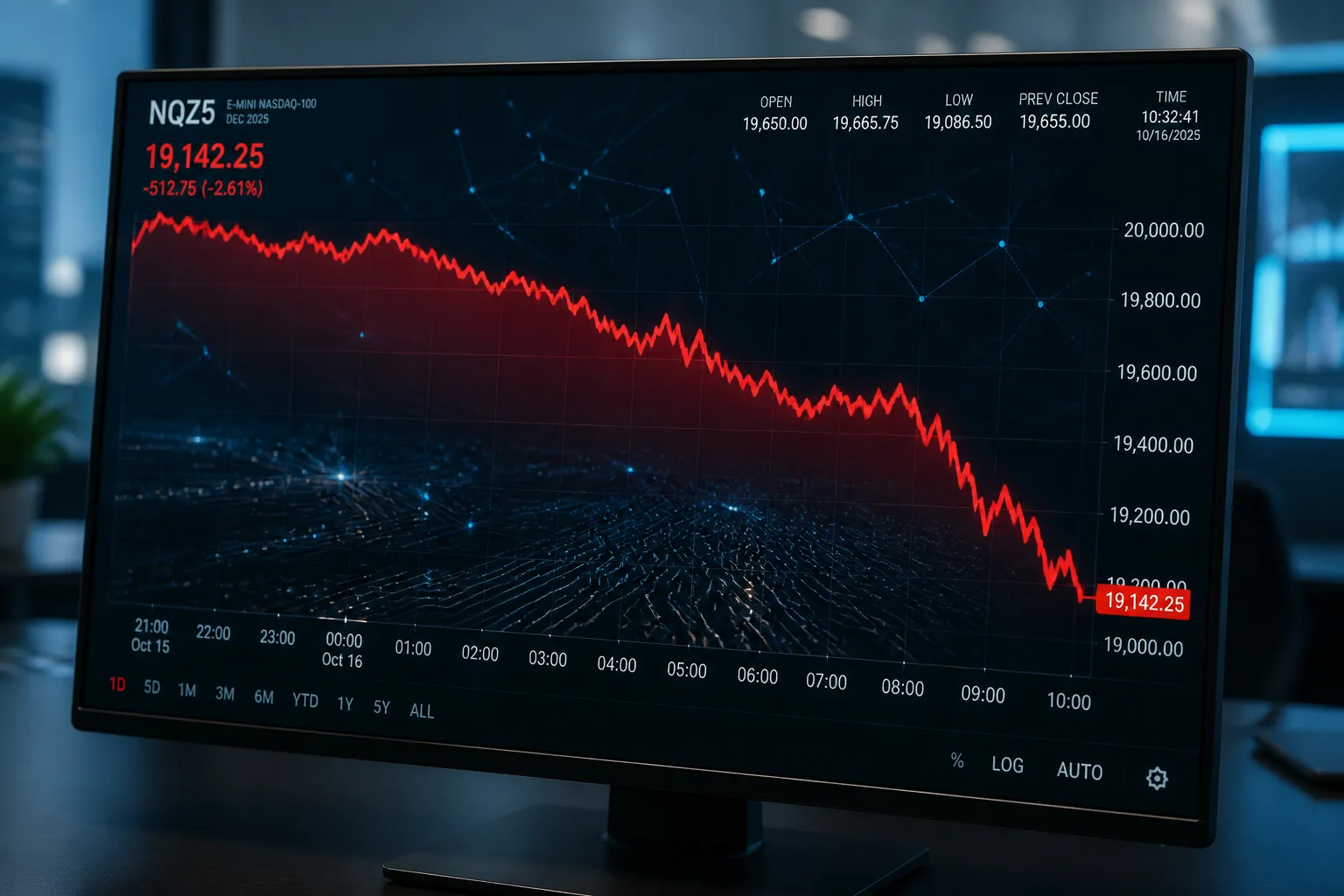

Last Friday’s market swing sent the technology‑heavy Nasdaq Composite down 4.2 percent, while the broader S&P 500 slipped 2.6 percent. The sharp pullback was largely driven by AI‑linked shares, prompting analysts to question whether the three‑year‑old boom has reached its apex.

The retreat has reignited worries that AI valuations grew too quickly. Some commentators have dubbed the drop a “semiconductor wipeout,” a term that describes how a sudden correction in one tech segment can drag down related industries. The comparison to the dot‑com era is frequently cited; former Federal Reserve chairman Alan Greenspan famously labeled that period “irrational exuberance.” Yet the current AI surge differs in scale and speed, and some observers warn it could be even more volatile.

The bubble narrative is not new. In the 1990s, online grocery startup Webvan raised nearly $400 million in venture capital, went public at the height of the dot‑com boom, and filed for bankruptcy in 2001 after spending $1.2 billion on warehouses and delivery trucks. That story illustrates how rapid investment can outpace the development of a sustainable business model.

Today, investors face four key realities that challenge the assumptions that fueled the recent rally:

1. High cost of AI – CEOs and companies such as Microsoft have acknowledged that building and deploying AI systems is expensive. 2. Limited immediate returns – A Bain study found that AI investments are not delivering profits at the pace many had expected. 3. Modest infrastructure demand – Broadcom’s latest forecast indicates that the demand for chips and memory to support AI workloads is weaker than the most optimistic projections. 4. Rising financing costs – The Federal Reserve’s trajectory of higher interest rates is expected to make borrowing for AI infrastructure more costly.

These factors undermine the narrative that AI can produce rapid, high‑yield returns. The U.S. stock market, built on the expectation of quick profitability, may find it difficult to justify the 1,000 percent+ gains seen in chip and memory stocks if the underlying business case weakens.

Annex Wealth Management’s chief economic strategist, Brian Jacobsen, noted that “recent earnings reactions suggest that even outstanding growth isn’t always enough when expectations are stretched— a classic ‘priced for perfection’ dynamic.” He added that some sectors still offer reasonable expectations and that valuations may provide a cushion.

Ben Berkoitz of Axios observed that “every great new technology has its moment where the business behind it resets, even as the tech itself keeps advancing.” His comment signals that the industry may be entering a phase where the business model surrounding AI is recalibrated.

Safety and governance concerns also loom. Andrea Morris, writing for Forbes, warned that “the most dangerous assumption in AI safety is that we can control AI once it’s smarter than us.” She added that because AI is a digitally distributed utility, it “can’t be governed like human cloning or nuclear arms development.” Morris suggests that market forces and corporate self‑regulation may eventually temper the pace of AI development.

The current market environment reflects a tension between the excitement of generative AI breakthroughs and the practical realities of deploying those technologies at scale. While the long‑term potential of AI remains strong, the recent retreat underscores the need for investors and companies to align expectations with realistic timelines and cost structures.

As the market digests these signals, the next weeks will likely reveal whether AI stocks stabilize, continue to decline, or find a new equilibrium that balances hype with sustainable business outcomes.

The retreat has reignited worries that AI valuations grew too quickly. Some commentators have dubbed the drop a “semiconductor wipeout,” a term that describes how a sudden correction in one tech segment can drag down related industries. The comparison to the dot‑com era is frequently cited; former Federal Reserve chairman Alan Greenspan famously labeled that period “irrational exuberance.” Yet the current AI surge differs in scale and speed, and some observers warn it could be even more volatile.

The bubble narrative is not new. In the 1990s, online grocery startup Webvan raised nearly $400 million in venture capital, went public at the height of the dot‑com boom, and filed for bankruptcy in 2001 after spending $1.2 billion on warehouses and delivery trucks. That story illustrates how rapid investment can outpace the development of a sustainable business model.

Today, investors face four key realities that challenge the assumptions that fueled the recent rally:

1. High cost of AI – CEOs and companies such as Microsoft have acknowledged that building and deploying AI systems is expensive. 2. Limited immediate returns – A Bain study found that AI investments are not delivering profits at the pace many had expected. 3. Modest infrastructure demand – Broadcom’s latest forecast indicates that the demand for chips and memory to support AI workloads is weaker than the most optimistic projections. 4. Rising financing costs – The Federal Reserve’s trajectory of higher interest rates is expected to make borrowing for AI infrastructure more costly.

These factors undermine the narrative that AI can produce rapid, high‑yield returns. The U.S. stock market, built on the expectation of quick profitability, may find it difficult to justify the 1,000 percent+ gains seen in chip and memory stocks if the underlying business case weakens.

Annex Wealth Management’s chief economic strategist, Brian Jacobsen, noted that “recent earnings reactions suggest that even outstanding growth isn’t always enough when expectations are stretched— a classic ‘priced for perfection’ dynamic.” He added that some sectors still offer reasonable expectations and that valuations may provide a cushion.

Ben Berkoitz of Axios observed that “every great new technology has its moment where the business behind it resets, even as the tech itself keeps advancing.” His comment signals that the industry may be entering a phase where the business model surrounding AI is recalibrated.

Safety and governance concerns also loom. Andrea Morris, writing for Forbes, warned that “the most dangerous assumption in AI safety is that we can control AI once it’s smarter than us.” She added that because AI is a digitally distributed utility, it “can’t be governed like human cloning or nuclear arms development.” Morris suggests that market forces and corporate self‑regulation may eventually temper the pace of AI development.

The current market environment reflects a tension between the excitement of generative AI breakthroughs and the practical realities of deploying those technologies at scale. While the long‑term potential of AI remains strong, the recent retreat underscores the need for investors and companies to align expectations with realistic timelines and cost structures.

As the market digests these signals, the next weeks will likely reveal whether AI stocks stabilize, continue to decline, or find a new equilibrium that balances hype with sustainable business outcomes.